DEMAND

The relationship between demand and prices is always in inverse. When prices go up, people buy less. When prices go down, they'd buy more.

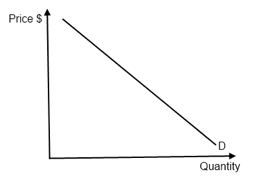

What is demand?

Demand is the quantity that buyers are willing to able to buy at various prices.

Here is an example of the demand graph. When the price is at its highest, the quantity demanded is at its least. So the cause in change of quantity demanded is the price.

What causes a "change in demand"?

- Change in buyer taste

- Change in population

- Change in income

- Change in price of related goods:

+Substitute goods: goods that serve the same purpose (i.e. cheetos, funyuns)

+Complimentary goods: goods that often consumed together (i.e. tortilla chips, salsa)

- Change in expectation

Normal goods and Inferior goods:

Normal goods: good that buy buy more of when income rise (i.e. beef)

Inferior goods: good that buyer buy less of when income rise (i.e. spam)

SUPPLY

Supply is different from demand, producers want to sell more with a high price. So it is a direct relationship between price and quantity supply.

What is supply?

Supply is a quantity that producer or seller are willing and able to produce/sell at various prices.

The supply graph above shows the direct relationship between its price and quantity. Ex: the more land you buy, the more it cost you to pay. So the cause in change of quantity supplied is when the price change.

What causes a change in supply?

- Change in technology

- Change in taxes of subsidies

- Change in number of sellers

- Change in resource prices/cost of production

- Change in weather

- Change in expectation

ELASTICITY OF DEMAND

The elasticity of demand tell how drastically a buyer will cut back or buy more

Elastic demand : E > 1

A product that is elastic when demand will change greatly give small change in price. (want)

Inelastic demand: E < 1

Demand will not change regardless of price. (need)

Unit elastic: E = 1

Here we have the formula for the Price Elasticity of Demand (PED)

1. (new quantity - old quantity) / old quantity

2. (new price- old price) / old price

3. step 1 / step 2 = PED [take the absolute value only]